Last updated: 8 July 2026 — covering June 2026 with a July outlook. This is a living page: we refresh it every month, so bookmark it for the latest China→USA rates.

June 2026

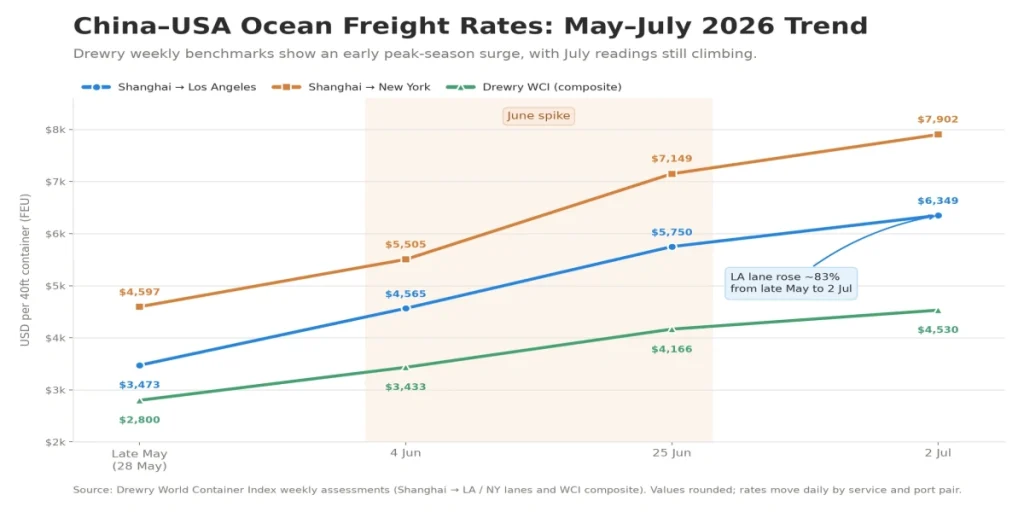

📌TL;DR — June 2026. China→USA ocean rates surged as peak season arrived about three weeks early. Drewry’s WCI rose from ~$2,800/FEU at the end of May to ~$4,166/FEU by 25 June, while Shanghai→LA reached ~$5,750 and Shanghai→NY reached ~$7,149. The move was driven by frontloading before July GRIs/PSS, tariff uncertainty, tight capacity and Red Sea / Hormuz routing pressure. July opened even higher, so importers should book early and budget for elevated mid-summer rates.

Quick summary

- Peak season arrived early, and the June rate spike was mainly a timing + capacity story.

- East Coast remained much more expensive than West Coast because all-water routings stayed tight.

- July is still elevated, but relief may appear later if frontloading fades and capacity returns.

Key rate snapshot

The headline: peak season came early

June turned a steady climb into a spike. The main reason was timing, not a demand explosion: importers pulled shipments forward before July fuel adjustments, GRIs, PSS and tariff uncertainty.

The market moved firmly into carriers’ hands. Drewry’s WCI jumped +23% to $3,433 on 4 June and reached about $4,166 by 25 June, while SCFI posted its ninth straight weekly gain to around 3,240 points. For shippers, the takeaway is simple: June delays quickly became expensive, and confirmed space mattered as much as headline price.

Ocean freight: China → USA spot rates (June 2026)

| Lane | Typical spot range (40ft / FEU) | Direction in June |

|---|---|---|

| Shanghai → Los Angeles (US West Coast) | ~$4,500–$5,800 | Rising sharply |

| Shanghai → New York (US East Coast) | ~$6,500–$7,200 | Rising sharply |

- West Coast climbed from ~$4,565/FEU in early June to ~$5,750/FEU by 25 June.

- East Coast stayed roughly $1,400/FEU higher because all-water capacity remained tighter.

- 20ft containers generally priced 10–20% below 40HQ, while transit times stayed around ~15–35 days depending on port pair and service.

Air & express: firm and elevated

Air freight stayed expensive through June, with China→US rates in the high single digits per kg. Use air or express mainly for time-critical, high-value-density cargo; keep bulk volume on ocean where possible.

| Air segment | Indicative rate (China → US) | Best for |

|---|---|---|

| Heavy consignments (100kg+) | High single digits per kg (lower end) | Larger urgent shipments where unit cost matters |

| Small parcels (sub-100kg) | High single digits per kg (premium) | Time-critical, high-value-density cargo |

What drove the market in June

| Driver | Signal | Impact | Importer meaning |

|---|---|---|---|

| Frontloading | Cargo pulled before July | Demand compressed into June | Book earlier |

| PSS / GRI | $2,000–$3,000/FEU increases | All-in cost rose fast | Compare all-in quotes |

| Capacity control | Blank sailings + rationed space | Less room for late bookings | Lock allocation |

| Routing drag | Red Sea / Hormuz pressure | Higher cost floor | Add buffer |

- Carrier surcharge and GRI details Carrier / measure Type Amount Effective Maersk PSS $2,000/FEU 17 Jun 2026 ONE PSS $2,000/FEU June 2026 CMA CGM / ONE PSS (20ft) $500–$600 per 20ft June 2026 Trans-Pacific GRI GRI ~$1,500/FEU 1 Jul 2026 CMA CGM (Asia → US/Canada) PSS Peak-season surcharge 10 Jul 2026 HMM PSS $3,000/FEU 15 Jul 2026

- Benchmark details: what the indices showed

- Drewry’s World Container Index moved from about $2,800/FEU at the end of May to $3,433 on 4 June (+23% in one week), then reached about $4,166 by 25 June, the highest level since September 2024.

- S&P Global’s Platts Container Index jumped about 80% in the 30 days to 24 June, reaching its highest reading since April 2022.

- Asia→US East Coast and Asia→Mediterranean spot rates pushed past their 2024 Red Sea-crisis peaks.

- China’s SCFI posted its ninth straight weekly gain to around 3,240 points by 26 June, climbing back above the 3,200 mark.

- For a 200-container program, a one-week LA move from $5,134 to $5,750/FEU would add roughly $123K in freight cost.

- Policy and demand notes: why cargo moved early

- Importers frontloaded cargo before the 1 July bunker adjustment, July GRIs and possible tariff changes.

- Tariff risk became more concrete on 2 June, when the USTR proposed Section 301 duties of 10%–12.5% on 60 economies, including China, the EU and Japan, with a public hearing scheduled for 7 July.

- Retailers also replenished lean inventories ahead of Prime Day and mid-year promotional campaigns.

- The 2026 FIFA World Cup across the US, Canada and Mexico added pull for merchandise, apparel and host-city retail replenishment near gateways such as Los Angeles, New York/New Jersey and Miami.

- Together, these factors compressed demand into June rather than spreading it across the normal early-summer window.

- Capacity and routing notes: why space stayed tight

- Carriers continued using blank sailings and allocation control, with only limited extra loaders added during the spike.

- Priority loading often required a premium because base-rate space was rationed.

- Red Sea / Strait of Hormuz disruption kept long-haul routings stretched and bunker costs elevated.

- Roughly 300,000 TEU, or about 1% of global capacity, was estimated to be tied up around the Gulf while the market watched for Strait of Hormuz reopening.

- On the US side, CBP inspection pressure and slower turnarounds tied up equipment, adding to the effective capacity squeeze.

Port & congestion watch

Asia-side delays worsened in June as weather and vessel bunching hit several hubs. On the US side, intensified CBP inspections (5H / VACIS holds) kept some containers sitting longer at destination ports. The result: slow turnarounds amplified tight capacity and made late bookings more expensive.

Outlook: July stays expensive, but watch for a turn

Base case: rates remain elevated through mid-July as July GRIs and PSS feed into the market.

Upside risk: AI-server, liquid-cooling and electronics exports keep Trans-Pacific demand firm.

Downside risk: frontloading fades and extra capacity returns later in the summer.

| July signal | What it means |

|---|---|

| WCI ~$4,530 by 2 July | Market was still rising after June |

| Shanghai→LA ~$6,349 / Shanghai→NY ~$7,902 | Trans-Pacific lanes remained elevated |

| HMM $3,000/FEU PSS from 15 July | Carriers were still pushing increases |

| Potential late-summer relief | The spike may fade if frontloading eases |

What importers should do now

| Action | Why it matters |

|---|---|

| Book earlier than usual | Pull normal lead times forward 2–3 weeks; peak-season space tightens fast once GRIs and PSS land. |

| Lock in where you can | For steady volumes, secure contract/NAC space rather than riding the spot market into further spikes. |

| Compare quotes on the same scope | A port-to-port ocean rate, an LCL per-CBM rate and a door-to-door DDP rate are not the same number — align Incoterms before comparing. |

| Build a buffer | With rates volatile and surcharges stacking, add margin to landed-cost models and confirm duty/HS treatment before shipping. |

| Keep a mode mix | Use air/express selectively for SKUs that genuinely can’t wait, and keep the bulk on ocean. |

June FAQ

What were China–USA ocean freight rates in June 2026?

By late June, Shanghai to Los Angeles spot rates reached about $5,750/FEU and Shanghai to New York about $7,149/FEU (Drewry, week of 25 June). On a broader China to US East Coast basis, Freightos put rates near $7,880/FEU by late June — up about 62% in a month.

How fast did the market move, and how does it compare historically?

Very fast. S&P Global’s Platts Container Index rose about 80% in the 30 days to 24 June, its highest since April 2022, and Drewry’s WCI hit a 22-month high. Asia to Mediterranean rates also jumped about 47% to ~$6,431/FEU, showing the surge was global, not just Trans-Pacific.

Did US-bound demand really spike, or was it mostly timing?

Mostly timing. China’s overall exports rose 19.4% year-on-year in May 2026, while exports specifically to the US jumped about 35% — the strongest pace since early 2021 — as importers frontloaded ahead of July surcharges and possible tariffs.

What tariff change were importers front-running?

On 2 June 2026, the USTR proposed Section 301 duties of 10%–12.5% on imports from about 60 economies (including China, the EU and Japan), with a public hearing set for 7 July and the earlier temporary 10% tariff due to expire 24 July.

Will rates keep rising in July?

July opened higher still — WCI ~$4,530, Shanghai to LA ~$6,349 and Shanghai to NY ~$7,902 by 2 July — with fresh GRIs and PSS such as HMM’s $3,000/FEU from 15 July. Base case is elevated rates through mid-July, with possible relief later in summer if frontloading fades and capacity returns.

May rate snapshot

| Lane / index | Late-May read | Market direction |

|---|---|---|

| Shanghai → Los Angeles | ~$3,473/FEU | Rising |

| Shanghai → New York | ~$4,597/FEU | Rising |

| Drewry WCI composite | ~$2,800/FEU | Rising |

| China → US air freight | $6.5–$7.0/kg; sub-100kg often $8–$9/kg | Firm |

What mattered in May

| Driver | Why it mattered |

|---|---|

| Capacity tightening | May Day blank sailings removed roughly 25% of Trans-Pacific Eastbound slots. |

| Early frontloading | Importers moved earlier after the US–China tariff truce and ahead of peak season. |

| Routing and fuel pressure | Red Sea / Hormuz disruption and elevated fuel kept the cost floor high. |

| June GRI setup | Carriers announced large June increases of roughly $1,000–$3,000/FEU. |

What were China–USA ocean freight rates in May 2026?

Spot rates ran roughly $2,000–$3,500/FEU to the US West Coast and $3,300–$4,600/FEU to the US East Coast, with late-May Drewry benchmarks near $3,473 and $4,597.

Why did rates rise in May?

Mainly carrier-driven capacity tightening, early peak-season frontloading, Red Sea / Hormuz routing pressure and elevated fuel.

What was the market signal for June?

May looked like the warm-up. June GRIs and Peak Season Surcharges were already being announced, setting up a steeper climb.